Objectives

The project entitled Revolutionizing Loan Processing sets interconnected objectives for the lending experience and the officers who run it.

- Increasing Halan loans wallet

- Guiding loan officer managers to prioritize certain deals and how best to structure them

- Maintaining loan officer managers’ self-esteem and income

Who loan officers are

Six core responsibilities along the lending journey—shown as a timeline from first review to compliance.

Click a step to expand or collapse details

Loan officers review loan applications to determine if borrowers meet the lending requirements of the financial institution. They assess credit scores, income, employment history, and debt-to-income ratios to determine the borrower’s creditworthiness.

Loan officers verify information provided by borrowers on loan applications, such as income and employment history, to ensure accuracy and prevent fraud.

Loan officers work with borrowers to negotiate loan terms, such as interest rates and repayment schedules, that are favorable to both parties.

Loan officers process loan applications by gathering all required documentation and submitting the application to underwriting for approval.

Loan officers work with borrowers to answer questions, provide information, and offer guidance throughout the lending process.

Loan officers ensure that all lending practices are compliant with federal and state laws and regulations.

Overall, loan officers play a critical role in the lending process and help connect borrowers with the financing they need while protecting the interests of financial institutions.

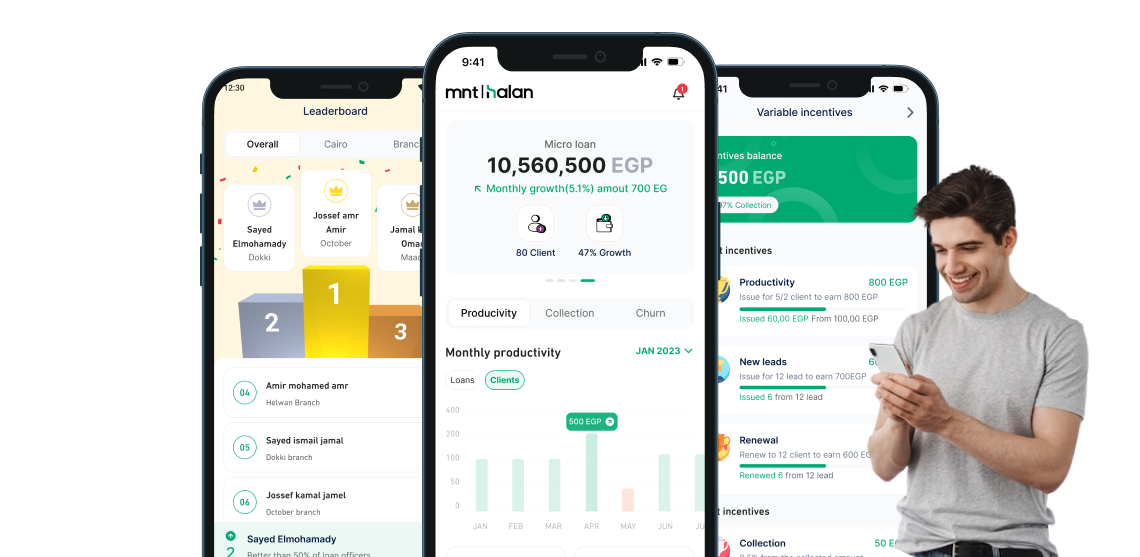

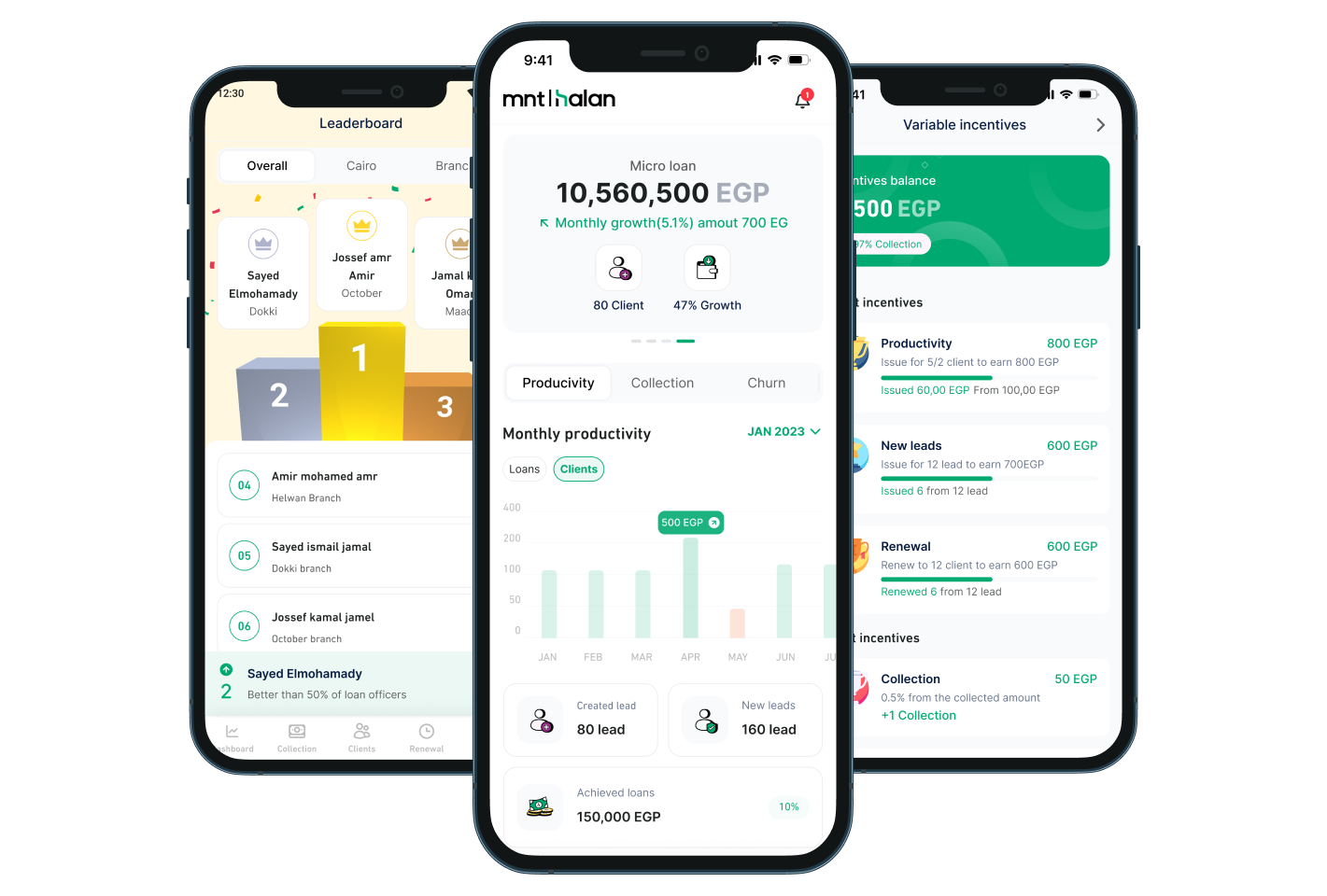

Revolutionizing loan processing

Hero composition from the MNT-Halan case study deck: dashboards, variable incentives, and officer-facing mobile UI.

What stops loan officers

from getting work done

Meeting lending quotas

Officers are often expected to meet lending quotas set by their institution, which can create pressure to approve loans that may be riskier than they should be.

Dealing with difficult customers

Officers may encounter customers who are unhappy with the lending process or who are not eligible for the loan they want.

Keeping up with changing regulations

Staying up to date with federal and state lending rules is complex and time-consuming.

Managing paperwork

Gathering and managing documentation from borrowers is time-consuming and tedious.

Evaluating risk

Each application requires sound judgment and a deep understanding of the borrower’s financial situation.

Competition

Competition from other institutions makes it harder to attract and retain borrowers.

Meeting customer expectations

Officers must help borrowers understand the process and terms—especially when expectations are high or borrowers are new to lending.

What we offer

loan officers

Gamification system

Increase the value of their work by adding a gamification layer and clear KPIs.

Income maintenance

Support salaries with variable incentives tied to measurable performance.

Online application

Let potential borrowers apply from home or office without always visiting a branch.

Automated underwriting

Use data-driven decisions to approve loans faster and more consistently, reducing manual bottlenecks.

Design strategy

Design strategy refers to an integrated planning process that examines how design and business complement one another. The goal is to merge business objectives with creative solutions that move beyond aesthetics.

Business goals

- Managing the loan lifecycle from application through approval and disbursement

- Streamlining processing, reducing errors, and improving efficiency

- Automating and simplifying day-to-day loan tasks

- Supporting credit analysis, interest calculations, and repayment monitoring

- Tracking performance: defaults, delinquencies, and key portfolio metrics

General tasks

- Loan application management: End-to-end application handling

- Creditworthiness analysis: Scores, income verification, debt-to-income

- Approval & disbursement: Documents, verification, fund release

- Collection management: Delinquencies, defaults, payment issues

- Reporting & analytics: Trends and data-driven decisions

Target users

- Loan officers: Processing applications, underwriting support, portfolio management

- Loan processors: Verifying borrower information and preparing loan documents

Cross-channel

Native Android and iOS mobile applications for officers in the field.

Critical success factors

- Efficiency: Streamlined tasks and fewer errors

- Accuracy: Reliable data on applications, approvals, repayments, collections

- Scalability: Room to grow with the business

- Integration: CRM, accounting, payments, and adjacent systems

- Security: Protection for sensitive borrower and lender data

- Flexibility: Different loan types and repayment models

- Reporting & analytics: Performance visibility for leadership

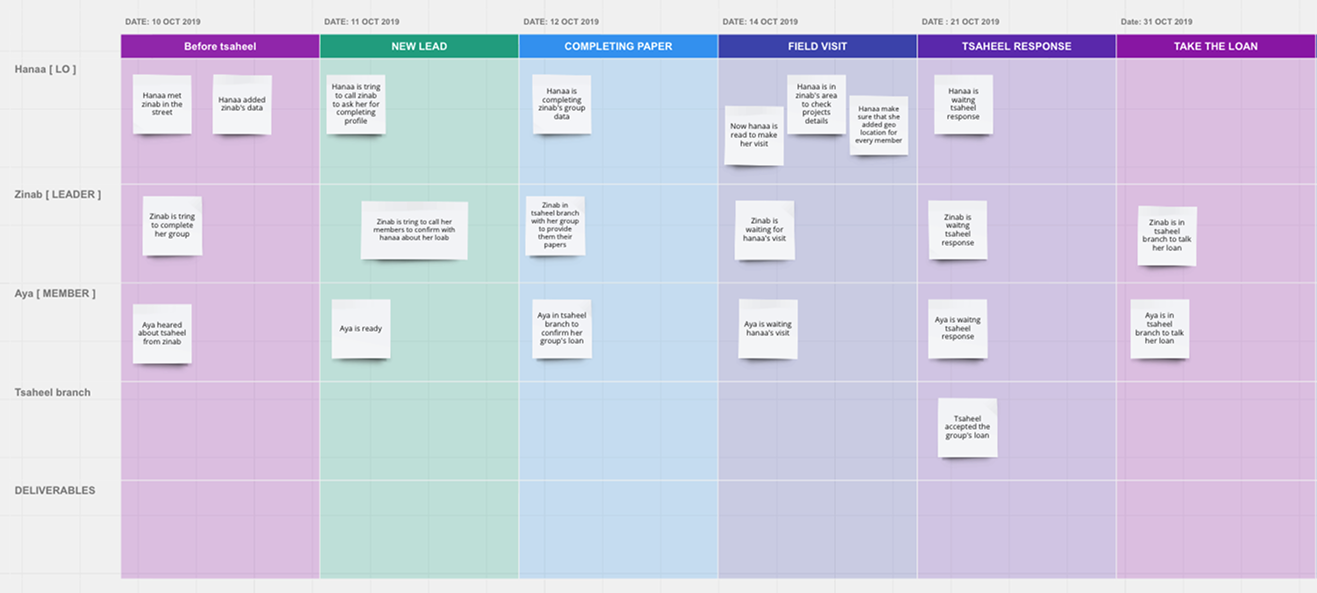

Timeline & process

Qualitative research included five stakeholder interviews to understand how teams coordinate lending work in the field—from group formation and documentation through visits and disbursement. The workshop board below captures roles, phases, and touchpoints across the journey (as documented in the case study).

Timeline & process / research board

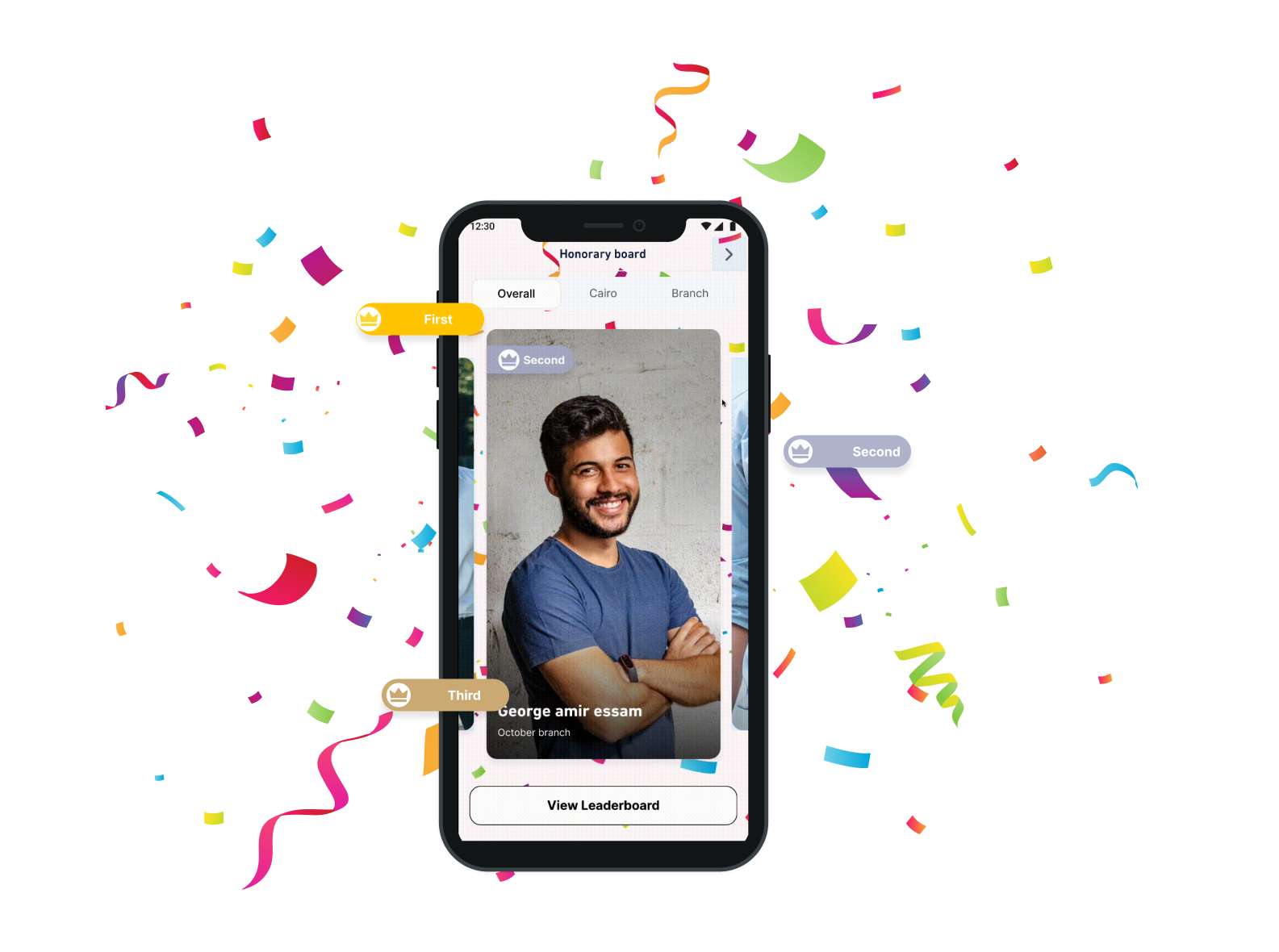

Managing lending,

collections & motivation

Native screens for micro-loan dashboards, monthly productivity, collection health, variable incentives, leaderboards, and honor boards—so officers see performance and earnings in one place.

Dashboards, installments & competition

Managing the lending system; tracking client installments; leaderboards and honor boards for healthy competition.

Golden booth & variable incentives

Highlight top performers monthly; surface target and direct incentives (productivity, new leads, renewals, collection, wallet growth).

Badges, recommendations & location

Achievements for clients, prioritized recommended actions for officers, and GPS-backed logging of client and project locations.

Intended outcomes

The product direction ties incentives and clarity of work to business goals: wallet growth, better deal prioritization, and sustained officer motivation—supported by automation and mobile-first workflows.

Takeaways

Motivation is a product surface

Gamification, leaderboards, and variable incentives must map cleanly to real KPIs or they erode trust with officers.

Field reality drives IA

Collection lists, installment states, and location checks mirror how officers actually move through a week—not only desk workflows.

Strategy before screens

Aligning business goals, tasks, users, and success factors early kept later UI decisions defensible to stakeholders.